Without question, divorce is one of the most difficult life transitions any of us can be called upon to make. No matter which partner initiates it, the process sends the participants and those who are closest to them through a passage that is emotionally and often legally harrowing. Further, the financial implications of divorce can be devastating, especially historically for women in transition. And when a marriage ends after 20 or more years—an increasingly frequent phenomenon known as “gray divorce”—the financial consequences for both partners may prove particularly difficult.

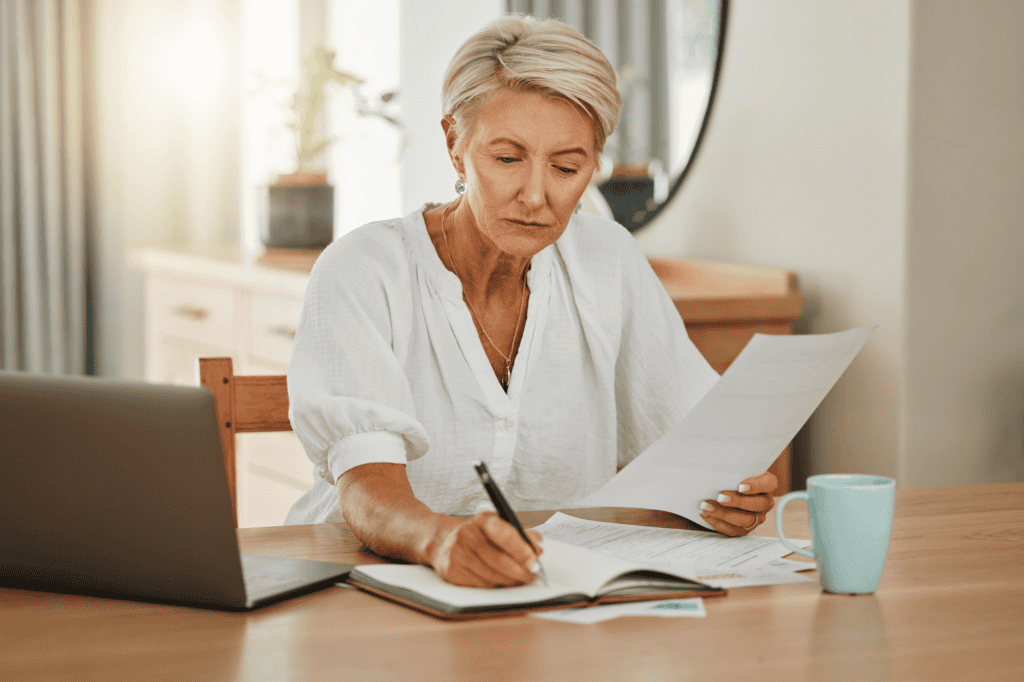

If for no other reason than the emotional upheaval generated by the divorce process, it is vital for both parties entering into divorce negotiations to have as much clarity as possible about what lies ahead, especially where the financial implications of dissolving a marriage are concerned. It can be helpful, then, to have some basic understandings of the major financial considerations surrounding divorce. After all, knowledge leads to confidence, and having financial clarity through divorce is one of the major predictors of the divorced person’s ability to successfully plan for this new phase of life.

1. Get informed. The first and most important step for financial planning during divorce is gaining the necessary information about the marital estate. It’s important to remember that unless it was included in a pre-nuptial agreement, property acquired during the marriage is considered to be owned by both spouses. It may be especially important for the spouse who has been less involved with the family finances to know the extent of the household’s assets, including the value of the family home and other real estate, the ex-spouse’s retirement accounts (401Ks, IRAs, and pension plans), any businesses owned, and any other investment or banking accounts. The participants’ legal counsel should help them gain access to statements, contracts, and other documents, if an ex-spouse is reluctant to provide the information. Both parties have the need and the right to know this information in order to make sure that the eventual division of assets is equitable and sufficient to sustain their long-term financial needs.

2. Divorce and taxes. For almost every decision involving dividing the marital estate, the tax consequences should be carefully considered. For example, a fair and equitable settlement may require that one of the spouses will need to give some portion of one or more retirement accounts to the other. This could involve liquidating assets and distributing them to the other spouse. If a retirement account is distributed prior to age 59 ½, the distribution may be taxable unless the distribution is performed according to a qualified domestic relations order (QDRO) provided by the court. It’s also important, when dividing assets, to consider the different tax consequences attached to Traditional IRAs and 401Ks as opposed to Roth 401(k) and IRA accounts. These differences should be considered in light of each recipients’ tax brackets, both currently and in the future. The same might be said of accounts like deferred compensation, stock options, and other assets in employer-sponsored accounts.

3. Keeping or selling the marital home. As we have written previously, the marital home is often a major asset in the marital estate, and this can be another place where tax considerations become important. If the home is transferred to the sole ownership of one or the other of the spouses, there will generally not be a taxable event. The spouse who retains ownership will also retain the original cost basis of the home, and if they subsequently sell it, they will need to be conscious of the potential capital gain implications. In such cases the Section 121 home sale tax exclusion ($250,000 for single individuals; $500,000 for couples filing jointly) may provide some relief. On the other hand, considering selling the home prior to the divorce being finalized could be advantageous given the higher exclusion when married.

4. Trust your team. A professional, certified financial advisor, working in tandem with your attorney, can help you anticipate problems and ask the right questions in order to ensure that you’ll have the financial resources you need as you begin your new phase of life. Make sure that your team can answer your legal and financial questions clearly, completely, and in terms that you understand. The more you know, the more you can be in control of your new future.

At JFS Wealth Advisors, we understand the special financial considerations that go along with divorce. That’s why we launched our Divorce and Separation Planning Niche, aimed at providing compassionate, informed financial guidance for individuals navigating one of life’s most challenging transitions. If you or someone you know is facing the bewildering prospect of divorce, we are here to help.

Disclosure: JFS is not a law firm and does not provide legal services. These materials are for informational purposes only and should not be construed as legal advice. If you require legal advice, please consult with a licensed attorney.