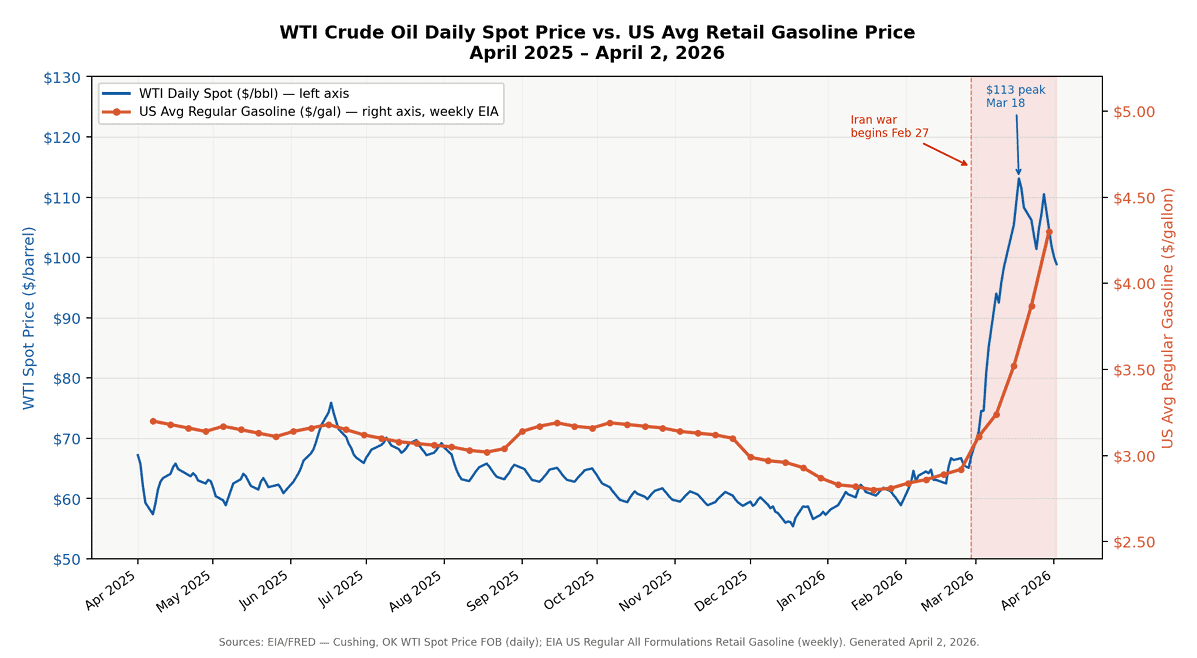

The first quarter of 2026 proved to be challenging for financial markets around the world. Following a generally positive beginning, the February 28 launch of U.S. and Israeli strikes against Iran impacted both stock and bond prices as oil prices soared and fears grew of a widening conflict.

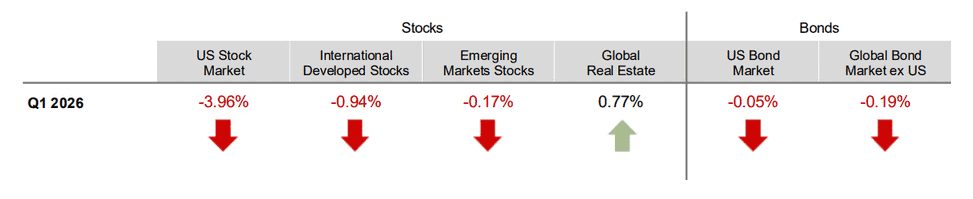

For the full quarter ending March 31, broad U.S. stocks as measured by the Russell 3000 index declined 4%, the S&P 500 fell 4.6%, and still bucking the trend, small U.S. companies as measured by the Russell 2000 rose 0.6%. Diversification continued to benefit portfolios, as developed international stock prices fell only 0.9%, and emerging markets slid 0.2%. On the fixed income side, pressured by worries of oil-price-induced inflation, U.S. bond prices treaded water, with the Bloomberg Barclays Aggregate essentially flat at a -0.05% return.

SOURCE: Dimensional Fund Advisors

US Stock Market (Russell 3000 Index), International Developed Stocks (MSCI World ex USA Index [net div.]), Emerging Markets (MSCI Emerging Markets Index [net div.]), Global Real Estate (S&P Global REIT Index [net div.]), US Bond Market (Bloomberg Barclays US Aggregate Bond Index), and Global Bond Market ex US (Bloomberg Barclays Global Aggregate ex-USD Bond Index [hedged to USD]) Past performance is no guarantee of future returns.

Benchmark Returns, as of Q1 2026

**Indices used for hypothetical portfolios returns are the MSCI ACWI for equities and the BBgBarc US Agg Bond for fixed income. All data derived from Morningstar Office. Past performance is no guarantee of future returns

The immediate impact of conflict in the Middle East is a worn playbook from prior oil shocks – spiking crude oil and gasoline costs (below), inflation fears, and global handwringing at the ease of disruption to world energy supplies. Yet it should be no surprise: the Strait of Hormuz has been a contested sea passage for centuries, and despite overwhelming air and sea firepower brought to bear against Iran, the dangers of hard-to-detect drones and missiles in the twenty-mile-wide strait can still effectively slam it closed. While renewable sources of energy continue to climb and are likely to see a surge following the recent events, petroleum products still drive some 80% of global energy consumption.

President Trump has indicated the U.S. and Israel will “finish the job” in Iran, while simultaneously seeking to calm markets by forecasting a short remaining window to the conflict. A tenuous ceasefire has just gone into effect, but no-one knows how the resolution looks. On the other hand, historical impacts from such a conflict tend to be limited if the duration is brief, and financial markets, while understandably volatile, are treating the events in that vein so far.

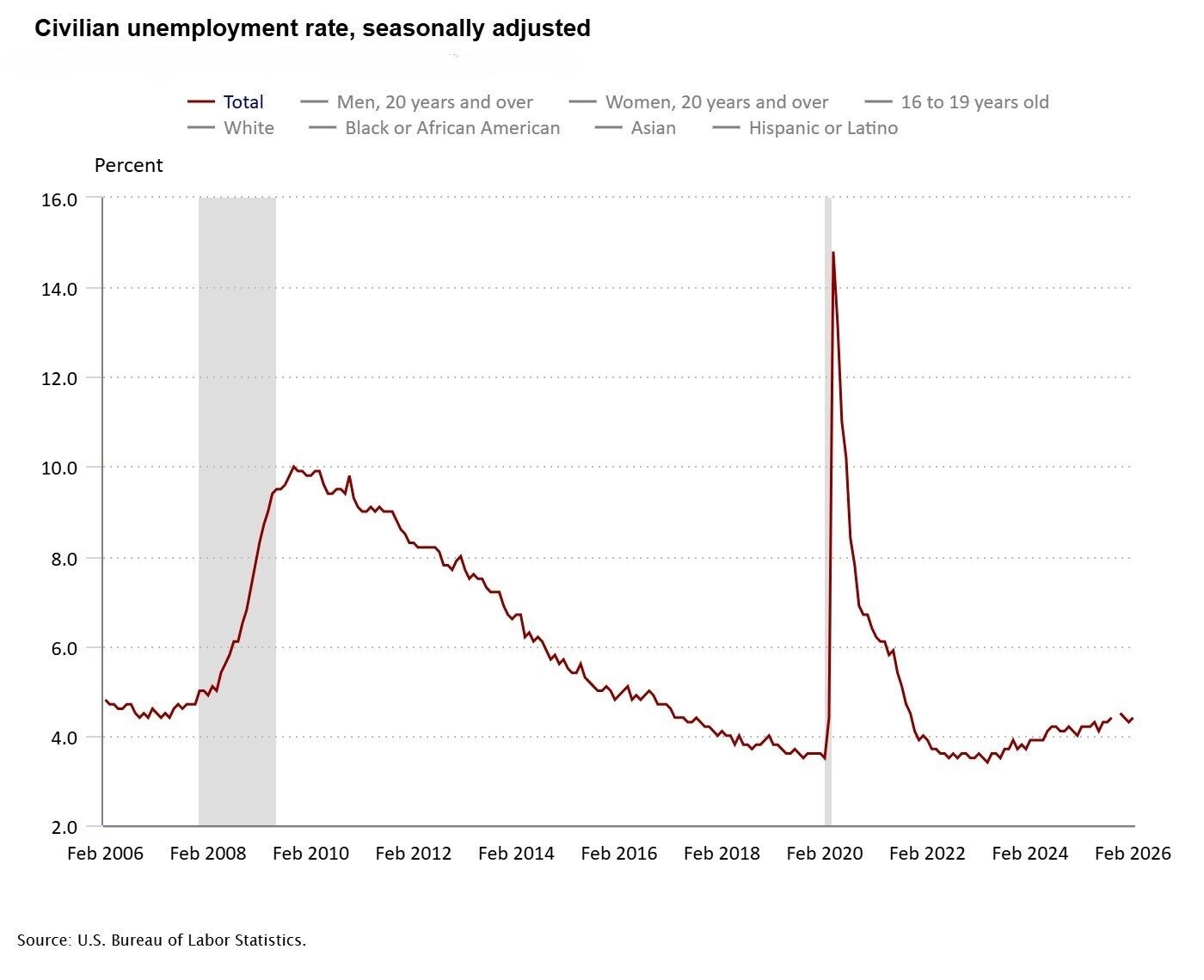

The U.S. economy has entered this highly uncertain period in a reasonably solid state. GDP for 2025 was 2.1% with some $30 trillion in output, and forecasts remain positive for 2026. As tax returns peak, early indications are that increased deductions are putting cash in taxpayers’ pockets, particularly in high tax states benefiting from the increase in SALT (State and Local Income Tax) deductions. The latest ISM Manufacturing report reflects a third month of growth, and the ISM Services report has grown for 21 consecutive months. And as the chart below shows, unemployment, while creeping higher from 2022 lows, sits at a still-attractive 4.3%. The most recent jobs report provided a positive surprise – 178,000 new non-farm jobs were created in March, with a bright spot of 15,000 new manufacturing positions.

Yet the details reflect rising challenges. The February jobs number was revised lower to a loss of 133,000 jobs, and the 3-month average to 68,000. The labor participation rate fell, but the reason was job searchers dropping out, indicating people have given up looking for work. There are some 6.9 million job openings, roughly matching the number of job seekers, with that ratio up from 0.5 just a few years ago. Meaning? A cooling labor market that has been coined “low-hire, low-fire.” And a significant unknown is the long-term effect of damage to global energy infrastructure from the Middle East hostilities. So, while the massive U.S. economy enters these troubled waters with forward momentum, Diane Swonk, Chief Economist at KPMG, voiced the rising worries of many as she recently noted, “We entered this year with a tailwind, and now that’s being wiped out by the headwinds.”

Global turmoil has momentarily shifted the spotlight away from Jerome Powell and the Federal Reserve, but likely not for long. The current Fed Funds target range is 3.5% – 3.75%, a level that is intended to account for a steady job market but stubborn inflation (CPI currently 2.4%). The already challenging balancing act will become even harder if oil prices remain elevated and subsequent inflation fully feeds through to an economy still absorbing tariff price pressures, and then growth stalls due to an energy shock. Recent comments from Powell reflect this high wire act: “Uncertainty about the economic outlook remains elevated. The implications of developments in the Middle East for the U.S. economy are uncertain. The Committee is attentive to the risks to both sides of its dual mandate.” Translation? “We (the Fed) have mandated goals that in a stagflationary environment are conflicting. Stand by as we work through this.”

And just to add spice to the mix, Kevin Warsh, President Trump’s pick as the next Fed Chair upon Powell’s May retirement, could face a bumpy road to confirmation. Senator Thom Tillis has vowed to block the nomination until the probe into Jerome Powell’s testimony surrounding renovation work at the Fed is completed. It is not a stretch to say that all eyes will be on the upcoming April 28–29 Fed meeting.

Stock markets are broadly maintaining the internal rotation that began in 2025. Value and small stocks continue to perform relatively better than growth and large stocks, and international markets, while certainly not immune to the Middle East problems, likewise continue to lead U.S. stocks for the year.

Yahoo Finance recently highlighted the Magnificent Seven companies that led the tech charge and how they are faring in 2026 to-date. At this writing, Alphabet (GOOG, GOOGL) was down 9% year- to-date. Amazon (AMZN) is down 8%. Meta (META) -12%. Microsoft (MSFT) -22%. Tesla (TSLA) -15%. Apple (AAPL) -6%, and Nvidia (NVDA) -8%. Certainly not a blood bath, but energy and industrials are now leading the pack, with bellwethers Chevron and Exxon gaining over 30% each. As we have noted many times, while it may seem boring, portfolio diversification continues to provide benefits.

Other data of note. Yields on the 10-year treasury increased slightly, ending the quarter at 4.31%. Crude oil prices leaped, closing on March 31 at $118.35/barrel. The price of gold had continued gains from 2025, closing the quarter at $4,647.60.

Private credit has lately been in the headlines as some private funds, facing redemption requests, have limited what investors can withdraw. Some articles point to this as the canary in the coal mine of broader fixed-income problems, but that seems unlikely. More likely is that many investors, lured by the siren call of market-beating yields, subscribed to these private funds not fully understanding either the risks or the redemption mechanisms. In thinly traded markets such as private loans, selling positions can take time and must be done carefully so as not to encounter forced discounts from buyers. Hence, many of these private funds provide limited liquidity windows and amounts so that shareholders are protected when someone wants to redeem shares. In short, they are illiquid! Investors should not be surprised, when they rush like lemmings for a nervous exit, that funds limit redemptions to preserve the value of holdings. It is a classic case of caveat emptor, and, at least for now, seems unlikely to spread beyond a small subset of fixed income.

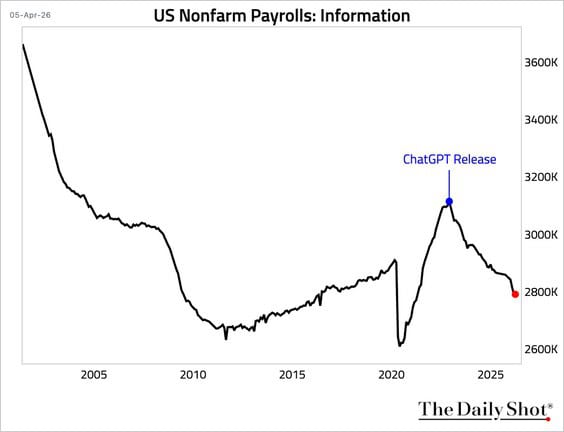

Another interesting aside is the ongoing impact of AI on the job market. Much speculation has surrounded the topic of AI replacing human workers. That is clearly occurring in some cases, but how far that goes remains uncertain. Nonetheless, the chart below provides a sobering look at job numbers in the information sector (software publishing, broadcasting, telecommunications, data processing, hosting, and publishing industries) following the release of ChatGPT. Caution must be taken in drawing a direct correlation between AI and job losses, but clearly something is happening. Efficiencies are gained when technology can be leveraged, often at the expense of human capital, and this seems likely to continue.

We all wish we had a crystal ball that would provide us a glimpse into what is to come – particularly when events are fast-moving. Yet being realistic and building all-weather financial plans and portfolios is all that we can do. French philosopher Voltaire noted that “Uncertainty is an uncomfortable position, but certainty is an absurd one.” So, amid volatility, please reach out to your JFS team with questions or concerns. We cannot predict the future for you, but we can certainly help you understand that patience and high-quality investments are the time-tested way to financial success and security, and that a solid financial plan can help keep you from making reactionary mistakes in times of stress.

Disclosure: Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by JFS Wealth Advisors, LLC [“JFS]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from JFS. JFS is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of the JFS’ current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at www.jfswa.com. Please Remember: If you are a JFS client, please contact JFS, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.