At the writing of our previous quarterly commentary, the government shutdown was unfolding and we noted, “For many government employees the effects are decidedly unpleasant, but if history is any guide, overall effect on financial markets should be muted.” That certainly was the case, as even though the shutdown proved to be the longest on record, financial markets around the world shrugged off the drama and closed the year on strong notes. And in a case of quarterly déjà vu, at this writing there is again significant breaking news, as the U.S. military has intervened in Venezuela and removed Nicolas Maduro from power. How these events will progress and their impact on oil markets and global economies is an unknown, but initial reactions suggest that markets are taking these events in stride.

Looking at the three months ending December 31, broad U.S. stocks as measured by the Russell 3000 index rose 2.4%, the S&P 500 gained the same amount, and small US companies as measured by the Russell 2000 climbed 1.9%. International developed markets saw stock prices continue their strong year, rising 5.2%, and emerging market stocks gained 4.7%. Bond prices rose as the Federal Reserve cut rates again in December, with the Bloomberg Barclays Aggregate up 1.1%.

The full year provided solid returns for those who stomached the uncertainty and stayed the course with their investment plans. While tech dominated headlines, diversification worked. The S&P 500 gained approximately 16% for the year (roughly 18% with reinvested dividends), the Nasdaq Composite rose 21%, and the Dow increased 13%, marking three consecutive years of double-digit returns. Helped by a falling dollar, developed international stocks rose an eye-catching 32%, and emerging markets 34%. Bonds gained 7.3% for the year, providing a solid boost as the ballast in balanced portfolios. Markets briefly flirted with bear market territory in April when the S&P 500 dropped nearly 20% following tariff announcements but subsequently staged one of the fastest recoveries since the 1950s, with stocks outside the U.S. leading the charge.

Source: Dimensional Fund Advisors

US Stock Market (Russell 3000 Index), International Developed Stocks (MSCI World ex USA Index [net div.]), Emerging Markets (MSCI Emerging Markets Index [net div.]), Global Real Estate (S&P Global REIT Index [net div.]), US Bond Market (Bloomberg Barclays US Aggregate Bond Index), and Global Bond Market ex US (Bloomberg Barclays Global Aggregate ex-USD Bond Index [hedged to USD]) Past performance is no guarantee of future returns.

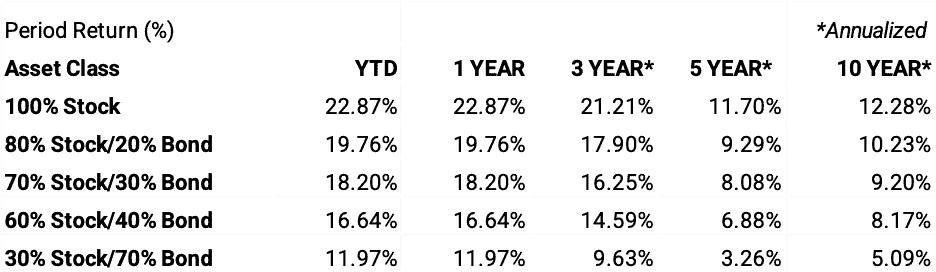

Benchmark Returns, as of Q4 2025

**Indices used for hypothetical portfolios returns are the MSCI ACWI for equities and the BBgBarc US Agg Bond for fixed income. All data derived from Morningstar Office. Past performance is no guarantee of future returns.

It is impossible to ignore the impact of AI when reflecting on 2025. While spending on generative AI still far exceeds revenue, the promise and increasing utilization of AI has been a driver of stock prices. Yet there are solid reasons to stay grounded and avoid chasing a single sector. The third consecutive year of gains in broad stock indices such as the S&P 500 masks the narrowness of the advance. Only seven stocks (The Mag 7) accounted for over 40% of the year’s gain, and according to Morningstar, over 60% of the gain was from just the IT and Communications sectors.

There are also other cautionary signs. In addition to the narrow concentration of returns, 2025 saw a returning flood of individual investor short-term trading. Meme stocks roared back to life, and trading via apps such as Robinhood dominated trading volume, accounting for some 75% of global retail trading. Direct retail ownership of stocks by individuals has fallen from over 90% in 1950 to under 30% today, yet in 2025 individual investors poured a record amount of cash into U.S. stocks, surpassing the “meme stock” frenzy levels of 2021. There has also been a surge in the trading of stock options by individuals. Peel that onion back another layer, and much of that volume was in the relatively new fad of zero-day options (0DTE), a high-risk bet on the price movement of an index or large ETFs such as SPY or QQQ … in a single day! They are cheap to buy but become worthless at the end of the trading day and are purely a bet on price movement in a matter of hours, the antithesis of long-term investing.

In addition to stocks, cryptocurrencies and tokens were in vogue, and Facebook pages dedicated to patrolling jewelry stores for silver and gold bargains and quick gains proliferated. For those of us with longer memories, the technology bubble of 1999 comes to mind. Remember the frenzy of people quitting their jobs to stay home and trade?

Taking a break from markets, economies around the world also climbed the proverbial wall of worry. The year began with uncertainty; tariffs and policy upheaval dominated. By May, U.S. tariffs had been imposed on over 70% of imported goods, with an effective rate peaking at over 17%. Yet as many levies were reduced or postponed, the effective rate has fallen to 11%, and the worst-case scenarios have not played out. As a result, actual growth exceeded consensus forecasts.

The December release of U.S. GDP data showed that real gross domestic product (GDP) increased at an annual rate of 4.3 percent in the third quarter of 2025 (July, August, and September), coming on the heels of a 3.8% increase in the second quarter. Imports (which subtract from GDP) have declined, exports increased, and consumer spending proved surprisingly resilient.

Globally, GDP growth for 2025 is projected to be 3.2%, which the World Bank attributes to significant AI investment, tame energy prices, and generally supportive central banks.

Yet, given the significant geopolitical upheaval around the world, increasing nationalism and decreasing globalization, and fractured foreign relations, a sense of unease remains. One of the most significant forward-looking measures, the Conference Board Leading Economic Indicators (LEI), portrays a slowing outlook. As noted in their recent release: “The LEI suggests slowing economic activity at the end of 2025 and into early 2026, with GDP weakening after strong mid-year consumer spending and Q4 disruptions amid the federal government shutdown. Overall, growth remains fragile and uneven as businesses adjust to tariff changes and softer consumer momentum.”

Consumer spending in the U.S. has become increasingly bifurcated, with high-income consumers leading the charge, while others have cut back due to inflationary pressures and a job market sending mixed signals. While, at 4.4%, unemployment remains low, the most recent jobs report for the month of December showed a weak 50,000 new jobs, below forecasts. The number of job openings is nearly 900,000 lower than a year ago, and while layoffs have not jumped, the weak hiring is sending a clear signal. In the face of an uncertain outlook, companies are in “low hire, low fire” mode, unwilling to make major commitments. It is leaving those outside of the wealthier status ranks with a sense of disquiet, and, like a volatile stock market, somewhat shell-shocked and anxious.

Another positive surprise for 2025 has been inflation. Traditional economics suggests a high correlation between tariffs and rising inflation, yet, while numbers remain above target in the U.S., the direst projections have not occurred. Why? Tariffs have been rolled back and postponed, forestalling the most dramatic levels, companies (many of which stocked up heavily before tariffs were imposed) have been reluctant to pass along the full costs yet, and consumers have been diligent in substituting less-expensive goods or just cutting back. CPI over the past months ending November is 2.7%, the lowest since July, and well below forecasts of 3.1%. While the government shutdown has muddied the data waters, at least for now, the inflation bogeyman remains under the bed, a positive for both bonds and stocks.

So, while the economic picture remains mixed, with stubborn inflation remaining in view, the Federal Reserve responded to the weaker labor and jobs outlook by cutting interest rates three times in 2025, bringing the federal funds rate to a range of 3.50–3.75%. But even the typically staid and opaque Federal Reserve is seeing volatile times as President Trump prepares to replace outgoing Chair Jerome Powell. It is no secret that this administration wants lower interest rates, and as this push filters into the Fed, we are seeing unprecedented internal division. There are 12 voting members of the Federal Reserve Open Market Committee, the group that meets eight times per year and sets monetary policy. Generally, they prefer to present a united front on their decisions, but in the December meeting there were three dissenting votes—the most since 2019. Expect more of the same as we move into 2026 and economic traditionalists face off against administration wishes. Entering 2026, the FOMC is heeding caution, with projections suggesting only one rate cut for the entire year Looking outside the U.S., central banks globally have continued gradual monetary easing, providing a generally benign backdrop.

Other items of note: The yield on the 10-year treasury ticked up slightly, ending the quarter at 4.16%. Crude oil prices fell again in the fourth quarter, declining nearly 8%. And despite Middle Eastern and South American uncertainty, oil and natural gas prices are remaining stable heading into 2026. Gold continued its run, gaining another 11.4% to close the year at $4,323.90.

The well-known economist John Kenneth Galbraith quipped, “The only function of economic forecasting is to make astrology look respectable.” So, while it is always entertaining to attempt to divine the coming movements of world affairs and markets, we know the more beneficial practice at the start of a New Year is to focus on data-driven facts and what history has proven to be true. A more appropriate quote to begin 2026 would be from Warren Buffet, where he noted, “Predicting rain doesn’t count, building the ark does.”

What does building an ark look like for growing wealth over time? Intelligently diversified portfolios tailored to match a personalized financial plan that is revisited frequently. While not the trading roller coaster depicted in the first cartoon, such an approach is far more likely to deliver financial success. Your JFS team has the tools, knowledge, and experience to help you design and stick to that plan. Please reach out to them with questions and updates.

2026 and beyond will deliver surprises, both positive and negative, and it is always tempting to try to anticipate and avoid market declines. Yet decades of experience and data suggest rewards come not from a perfect crystal ball, but rather from good, old-fashioned patience and common sense grounded in reality. Managing your assets in a steady plan that allows for short-term volatility and needs, while keeping an eye the horizon to build long-term security, all while ignoring the daily ups and downs and muting the 24/7 news cycle lets you sleep better at night and avoid costly and reactionary timing mistakes. On behalf of all of us, thank you for the trust you place in us, and Best Wishes for a Healthy, Happy, and Prosperous New Year.

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by JFS Wealth Advisors, LLC [“JFS]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from JFS. JFS is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of the JFS’ current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at www.jfswa.com. Please Remember: If you are a JFS client, please contact JFS, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.