The second quarter of 2026 reflected a robust rebound in financial markets from the uncertainty spawned by the Middle East conflict. A temporary ceasefire in April between the U.S. and Iran was followed by a signed 60-day extension on June 17, leading to declining crude oil prices and a general relief rally in risk assets. However, at this writing, Iran and the U.S. continue to trade fire in the Strait of Hormuz, bringing into question the durability of the supposed ceasefire and the likelihood of a successful resolution for the conflict. As hopes rise and fall around this issue, so go the financial markets.

For the three months ending June 30, broad U.S. stocks, as measured by the Russell 3000 Index, jumped 15.4%; the S&P 500 rose a similar amount; and small U.S. companies gained nearly 21%. The rally was global, as international developed stocks rose 10.2% and emerging markets continued their ascent, rising 24.1%. Bond prices stayed steady, gaining 0.7%, with the 10-year U.S. Treasury bond now yielding approximately 4.5%. Diversification beyond large-company tech was again a significant help; the Mag 7 stocks as a group returned less than 2% for the quarter. Gold prices fell slightly for the quarter, ending at $4,027 per ounce.

Source: Dimensional Fund Advisors

US Stock Market (Russell 3000 Index), International Developed Stocks (MSCI World ex USA Index [net div.]), Emerging Markets (MSCI Emerging Markets Index [net div.]), Global Real Estate (S&P Global REIT Index [net div.]), US Bond Market (Bloomberg Barclays US Aggregate Bond Index), and Global Bond Market ex US (Bloomberg Barclays Global Aggregate ex-USD Bond Index [hedged to USD]) Past performance is no guarantee of future returns.

Benchmark Returns, as of Q1 2026

**Indices used for hypothetical portfolios returns are the MSCI ACWI for equities and the BBgBarc US Agg Bond for fixed income. All data derived from Morningstar Office. Past performance is no guarantee of future returns

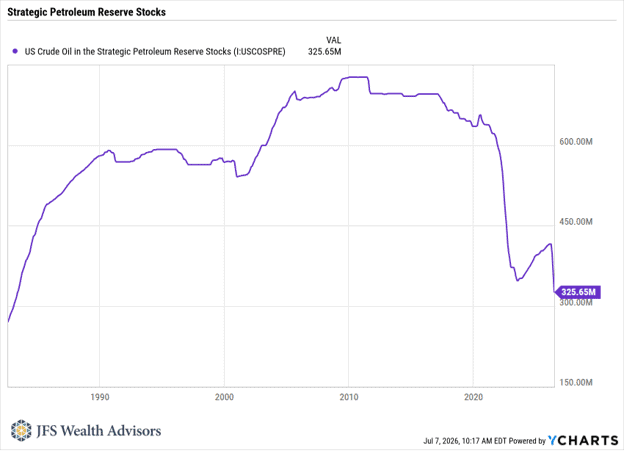

We noted in last quarter’s commentary that effects from regional conflicts, such as the U.S.–Iran war, tend to be temporary, despite scary headlines and pundit handwringing. To date, at least in most financial markets, that has proven to be the case. Yet there are longer-term implications, particularly in the world of energy. Free passage through the Strait of Hormuz is in doubt going forward, as Iran flexes its control over the narrow waterway and discusses a “maritime security agreement” with Oman concerning the Strait. Translation: an unwelcome exertion of control—and possibly even tolls—by the countries bordering the Strait, adding a risk premium to all shipping through the area. In addition, as supplies from the Middle East were restricted, global oil supplies in storage have fallen around the world. As the chart below shows, U.S. Strategic Petroleum Reserves are at their lowest level since the early 1980s, a trend mirrored around the world. So, while energy prices have fallen from their war-induced peaks, price pressure will continue as countries seek to rebuild these important reserves. Make no mistake: Iran is emboldened by its ability to affect shipping through the Strait and the leverage that ability has provided, despite being outgunned. Even if the ceasefire holds (more doubtful, given current developments), the eventual outcome of the war with Iran has set a new stage for persistent energy pricing pressure and supply constraints, compounded by a U.S. administration that is actively discouraging alternative energy buildouts.

Nevertheless, most economic data remained resilient throughout Q2. Manufacturing appears to be entering a nascent growth stage. The latest ISM Manufacturing report reflects six consecutive months of growth, albeit with near-term pressures; as one survey respondent noted, “Input costs remain elevated across key categories, driven largely by Middle East conflict impacts and ongoing tariff uncertainty. Supplier lead times have stretched, which is influencing our inventory strategy and sourcing decisions.” Increased domestic manufacturing is an unambiguous positive, though tempered by the fact that the majority reflects large-scale commitments from areas such as advanced technology, pharma, and semiconductor production, which are capital-heavy but labor-light. So, while firms are indeed “reshoring,” outside of the jobs needed for construction, don’t look for a labor boom from these new builds.

The services sector also continued to grow, as it has for some time, with the latest report showing 24 consecutive months of expansion. The ISM provided some context: “…supply chains are stabilizing amid sustained business activity, giving businesses confidence that selective, yet modest, increased employment is warranted. World Cup–related hiring in the U.S. likely contributed to the increase in the Employment Index. Of the 18 services industries, nine—representing over 58 percent of U.S. gross domestic product (GDP)—reported higher employment levels in June. This reflects widespread confidence that hiring is again warranted to support activity levels.”

The June jobs report, though slower than in previous months, showed a gain of 57,000 jobs, led by professional and business services, social assistance (family services, job training, childcare), and health care. Unemployment remains low, at 4.2%. Looking ahead, the Conference Board’s Index of Leading Economic Indicators (LEI) can be helpful in putting this all together. The June 18 LEI release reflects generally steady data in the face of external uncertainty. Comments from Justyna Zabinska-La Monica, Senior Manager of Business Cycle Indicators, capture this mixed picture: “Despite two consecutive monthly increases, the LEI’s six- and twelve-month growth rates were still negative, suggesting slower economic expansion ahead. Consumers are feeling squeezed because everyday costs—especially gas and energy—are rising faster than their incomes, leaving many households with less money available for things like travel, restaurants, entertainment, and shopping. The good news is that businesses are spending heavily on AI, data centers, and new technology, helping to keep the economy growing while consumers pull back spending. The overall job market is expected to stay fairly healthy in 2026, but economic growth will be weaker than in recent years. The Conference Board is currently projecting 1.8% y/y GDP growth in 2026, down from 2.1% in 2025.”

What about inflation? Put simply, it hurts. Highlighted by gasoline prices (+ 40.5% over the past 12 months), the Consumer Price Index climbed 4.2% over the 12 months ending May 31—the highest level in three years. The Producer Price Index, which reflects input prices, rose even more, up 6.5% over the same period. The good news is that energy prices are retreating from their highs, but price pressures across the board remain persistent. And, as noted above, energy prices are likely to stay elevated for some time, keeping inflation well above the Federal Reserve’s 2% target.

Given these inflation dynamics, new Fed Chair Kevin Warsh faces pressures of his own. It was a very short honeymoon. While President Trump has publicly called Warsh a “very good guy” and urged him to “do your own thing,” the President has also repeatedly and loudly called for lower interest rates, saying the current rate regime “keeps the country down.” Warsh is generally viewed as pro-business, but mainstream economists are skeptical of his credentials—he does not hold a Ph.D. in economics—and his elimination of forward guidance from the Fed has raised criticism and fears of market volatility. Unlike former Chair Powell, Warsh has been tight-lipped as he works to put his own imprint on the Fed. Given the importance of this role, expect some ups and downs as markets adjust to his unique approach and communication style.

On the topic of inflation, the Wall Street Journal recently ran an opinion piece titled “Why Everything Feels More Expensive,” by Harvard economics professor Roland Fryer. Fryer explores why so many families feel squeezed and dissatisfied, even though median family income has climbed roughly 55% since 1975 and productivity gains have raised living standards and life expectancy. The explanation lies in an economic concept known as Baumol’s Cost Disease: productivity gains (think technology) often translate into lower costs and higher quality for goods—unequivocally a good thing. But service industries such as childcare, healthcare, hospitality, and government, where the bulk of the product comes from human labor, see the opposite: higher costs and labor shortages. This hits home for most middle-class families, whose budgets are dominated by these kinds of expenses. As Fryer notes, safer and more reliable cars, cleaner air, widespread adoption of time-saving technology, and longer lives are all real gains, but they become taken for granted over time and overshadowed by the painful reality of budgets consumed by the costs of children, insurance, leisure, and taxes. This helps explain the frustration expressed by so many Americans today as they run ever faster on the treadmill just to keep pace.

❖

At this writing, we are just days past the July 4th celebration of the 250th anniversary of the adoption of the Declaration of Independence. Much has been written about the future of America—some positive, some negative—all of it competing for our attention as the defining narrative. The real story is, as you might expect, more nuanced, and worth taking a few moments to consider.

Deutsche Bank Research Institute released a report on June 24 titled “US at 250 – Why Has the US Been So Successful, and Can It Continue?” I’m not going to summarize the piece for you (AI can do that if you’d like) but given today’s polarized politics, the widening income inequality gap (see the Baumol’s Cost Disease discussion above), and the often-highlighted sense that the U.S. is losing its way as a beacon to the world, I do want to highlight three points.

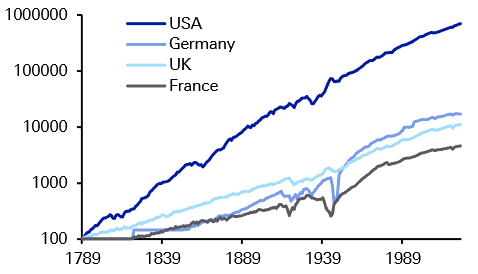

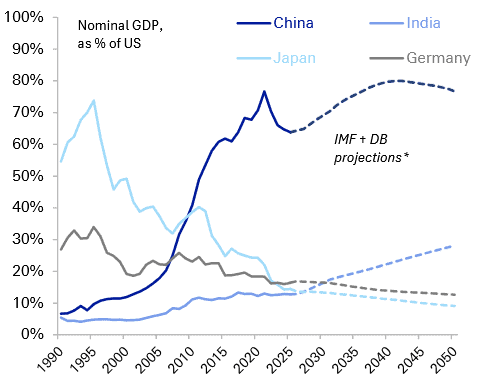

1) Economic growth has paved the road. Consider the first chart below: US growth in domestic output has far outpaced the world and has provided the underpinnings for a whole host of societal benefits. Capitalism certainly has its flaws, but an economy built around creativity and the pursuit of building wealth that can be shared with others is uniquely powerful. In more recent years the U.S. has increasingly shared the economic stage with China (second chart) but U.S. nominal GDP remains roughly $10 trillion greater, created less by government and more by individuals. And, arguably, social mobility and freedoms in the U.S. far surpass those in China.

Real GDP on a log scale (1789 = 100)

Source: Finaeon, Deutsch Bank

US likely to remain the world’s largest economy for the foreseeable future

Source: IMF World Economic Outlook, Deutsche Bank Research * IMF projections to 2031; DB estimate to 2050 based on (i) UN population projections (2024), (ii) stable productivity growth among DM economies, (iii) gradually slowing labour productivity growth for China (to 2.0% by 2050) and India (3.5% by 2050), (iv) stable REER exchange rates.

2) As a corollary to world-leading economic growth, the U.S. dollar has been—and remains—the world’s reserve currency, providing a similar host of benefits. Roughly 82.5% of global trade currency is denominated in U.S. dollars, resulting in lower borrowing costs for the U.S. and greater tolerance for budget deficits, which helps keep a lid on interest rates and the cost of government debt. The post–WWII order may indeed be changing, but for the foreseeable future, dollar dominance and the concurrent benefits remain.

3) Education and research have attracted exceptional talent to the U.S. Deutsche Bank notes that 7 of the world’s top 10 research universities are in the U.S. The discoveries and practical applications flowing out of U.S. universities, combined with open financial markets and abundant sources of funding, have driven U.S. leadership in many areas, with technology as the poster child.

An important editorial note: Rebuttals can be made to all these points; blind optimism is not in order here. But neither is a persistent focus on the negatives. American exceptionalism is real, and the experiment begun on these shores 250 years ago has produced a society unlike any other. Having spent the first thirteen years of my life living overseas, I speak with experience to the amazement in encountering so many things that Americans assume as normal that are luxuries or downright inaccessible when outside these shores. Anecdotally, the FIFA World Cup has brought a host of happily surprised first-time visitors extolling on social media many facets of daily American life that we take for granted. But this is not to say everything in this country is perfect and without problems—far from it. The positives do not mean the many economic and social challenges we face are not real and growing. Patriotism can mean different things to different people, but a shared sense of obligation to make our country better for all should be common ground. Happy 250th, America!

The Deutsche Bank piece has far more content than touched on above, is publicly available, and worth a read. If you’re interested, please let us know and we’ll send you the link.

❖

As we move deeper into summer, we wish you some rest and relaxation before the busy days of fall appear. As a firm, reflecting on our fortieth anniversary of working with exceptional clients, and on behalf of all my JFS colleagues, we want to express our appreciation for your confidence. We take our commitments to you seriously and are gratified by the trust you place in us. Please reach out to your JFS team with any questions.

Disclosure: Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by JFS Wealth Advisors, LLC [“JFS]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from JFS. JFS is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of the JFS’ current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at www.jfswa.com. Please Remember: If you are a JFS client, please contact JFS, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.